.webp)

Underwriting and broking talent continues to flow into the MGA sector, and with it a high level of knowledge and innovation.

The MGA model represents a preferred distribution method for many products, both simple and complex throughout the market.

Delegated authority now represents over 40% of the Lloyd’s market’s volumes. In the broader UK general insurance space, more than 350 MGAs are underwriting over 10% of the UK’s £47 billion general insurance premiums.

Whilst the MGA model is attainable, MGAs are required to navigate:

- High barriers to entry for first-time MGAs without performance history or credible proof of concept

- Regulatory and licensing hurdles

- Carrier oversight burden and friction

- Changing capacity appetite, as carriers shift strategic focus or risk appetite

MGAs that master these 3 fundamentals will be best positioned to unlock market opportunities.

What UK MGAs need to win in 2025 and beyond

1. Capacity will always be king

The importance of the capacity provider - the coverholder/MGA relationship will always be a key component of the marketplace.

Fortunately, appetite for capacity allocation remains strong in the UK.

In the 2025 MGA Opinion Report, 46% of carriers reported increasing their capacity allocation to MGAs in the last 12 months, and 57% of carriers expect their capacity allocations to MGAs to increase by 5% in the next two years. Carriers are also looking to provide capacity to MGAs to offer new lines of business, with speciality lines (29%) and financial lines (20%) being focus areas.

Securing long-term capacity, where possible, can help MGAs avoid the uncertainty of short-term capacity constraints, especially in hard markets.

A multi-carrier approach can also mitigate the risks of a single carrier relationship. However, carrier relationships come with associated overhead, and this should be kept in mind when considering a multi-carrier approach.

Delegated authority works best when capacity providers trust the performance, controls, and data of MGAs.

2. Data integrity is a competitive advantage

The importance of data extends beyond reporting; it means credibility in every capacity meeting, audit and renewal. Data integrity that stands up to scrutiny provides the best chance of obtaining top tier capacity.

In fact, 75% of carriers surveyed by the MGAA cited expertise and data to ensure good risk selection and pricing as their top requirement for potential MGA partners.

Data expectations can vary wildly between capacity providers, auditors and regulators. MGAs have to be ready to satisfy them all. The problem is compounded when data is siloed in different, fragmented systems with no/limited interoperability between them.

From a regulatory perspective, demonstrating compliance with Consumer Duty will also need to be supported by integrated data governance.

When data is late, inconsistent, or siloed, you lose trust, flexibility, bargaining power, and eventually capacity. This is where a slick, robust tech stack is pivotal.

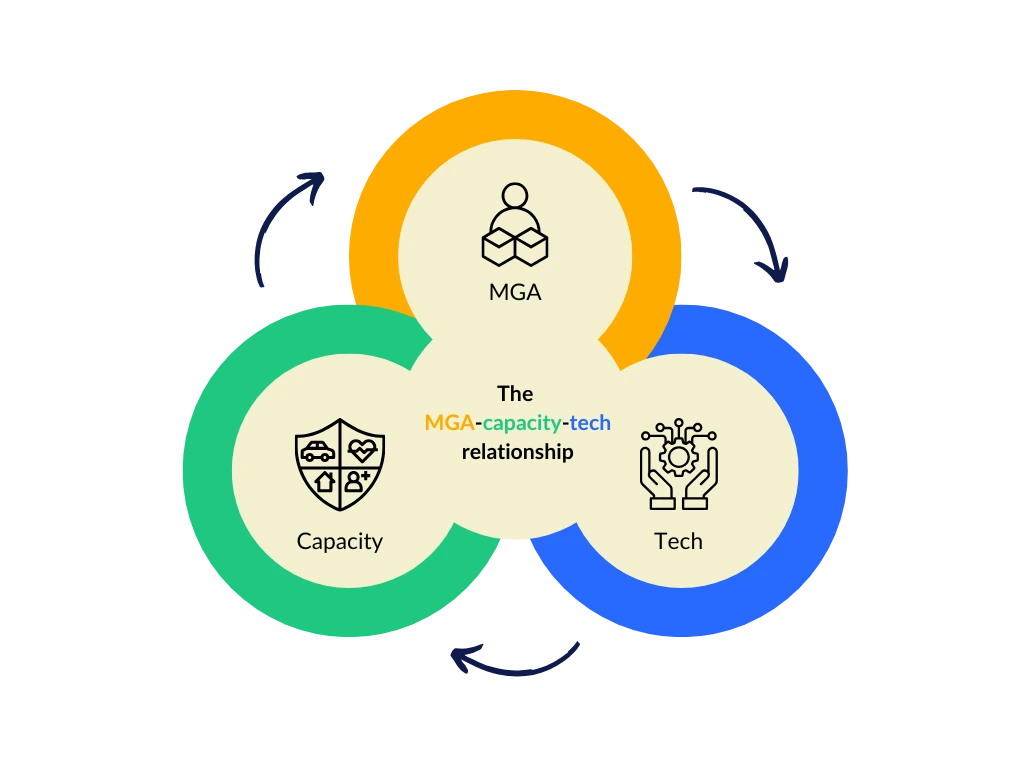

3. Marrying tech, capacity and MGA expertise

In an ideal state, MGAs, capacity providers and technology co-exist in a synchronous, tripartite relationship, moving forward together in lockstep.

When all three align, growth accelerates. MGAs bring product expertise and market access. Capacity providers bring financial strength and credibility. And technology ties it all together, providing the data, control and visibility that allow the partnership to scale with confidence.

The reality is that capacity flows where trust flows. Tech builds that trust. When data is transparent, governance automated and oversight effortless, capacity providers gain the confidence to back MGAs more boldly.

That’s why the right technology partner isn’t just a vendor. They’re a growth ally - one that enables MGAs to underwrite smarter, move faster and operate with greater control.

Moreover, the technology platform underpinning the value chain must be built to earn trust, enable scale, deliver flexibility and facilitate control. Only then does tech become a competitive advantage rather than a cost.

What to demand from your tech stack:

- API-first infrastructure: to integrate with carriers, data providers, compliance, claims engines, pricing models without re-architecting.

- Unified data management: all systems (policy admin, underwriting, claims) feed into a normalised, auditable policy administration system.

- Modular / integratable services: ability to switch out modules (e.g. claims, underwriting) as business evolves without needing to replace the entire tech stack.

- Scalable, cloud-based infrastructure: for handling spikes, expansion, international lines, or new product classes.

- Security, audit trails, compliance frameworks: these are imperative in a tightly regulated market.

- Embedded dashboards & analytics: for both MGA and capacity partners to monitor performance, trends, exceptions.

The MGA boom

The MGA model continues to gather pace in the UK.

Scale is no longer the challenge - control is. Those who unite capacity, data and technology into one seamless ecosystem will define the next decade of growth. Because when trust, transparency and technology align, the future of insurance becomes not just possible, but inevitable.

If your tech is reliable and extensible, it becomes a pillar of trust - and that helps you thrive in capacity conversations, audits, renewals as well as expansions.